Updated June 2020

Further to the article below, HMRC have announced that the changes will now not take effect until 1 March 2021.

VAT Alert - Summer 2019

From 1 October 2019, if your VAT-registered business provides construction services to another business you will no longer need to charge them VAT. This is because your customer will need to account for it under the new domestic reverse charge.

This reverse charge will affect the supply of building and construction services whether they are supplied at the standard or reduced VAT rates which also need to be reported under Construction Industry Scheme 'CIS' rules. Supplies between sub-contractors and contractors (as defined by CIS) will also be subject to the reverse charge, unless the recipient is an end-user.

An ‘end-user’ is defined as a recipient who will use the services for themselves rather than selling them on. This distinction is important because supplies made to end-users will continue to be subject to a VAT charge. You must check contracts to determine who the work is being carried out for.

What if I am a contractor?

As a contractor you will need to review all of your contracts with sub-contractors to decide if the reverse charge will apply. You will need to notify your suppliers accordingly.

What if I am a sub-contractor?

You will need to contact your customers to get confirmation from them if the reverse charge will apply, you will also need to confirm if the customer is an end-user.

If the domestic reverse charge applies then you must:

- Show all the information normally required to be shown on a VAT invoice

- Annotate the invoice to make clear that the domestic reverse charge applies and that the customer is required to account for the VAT

The amount of VAT due under the domestic reverse charge should be clearly stated on the invoice but should not be included in the amount shown as 'total VAT charged'.

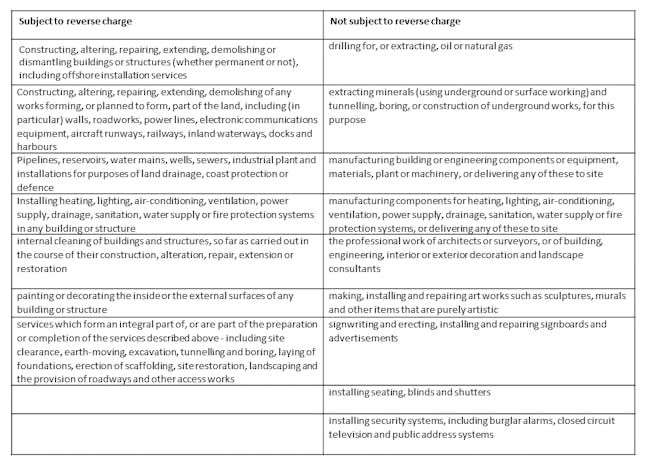

The following table gives details of where the reverse charge does and does not apply:

End-users and intermediary suppliers

The reverse charge does not apply to intermediary suppliers – that is if a number of connected businesses collaborate to purchase construction services. They would all be treated as if they are the end-users. Intermediary suppliers are VAT and CIS registered businesses connected to end-users who:

- share a relevant interest in the same land where the construction works are taking place; and

- belong to the same corporate group or undertaking

HMRC suggests a practical way of dealing with the question of end-user status would be for businesses to include a statement in their terms and conditions to say they will assume their customer is an end-user, unless they say they are not.

HMRC acknowledges that some businesses which have large numbers of active contracts with sub-contractors at a variety of sites, may have difficulty establishing whether the reverse charge applies or not in the run-up to 1 October 2019. The guidance therefore states that where contractors can see that the reverse charge applies to more than 5% (by volume or value) of all contracts with a particular sub-contractor, they may apply the reverse charge to all contracts with that sub-contractor.

Transitional arrangements mean that normal VAT rules will apply to invoices for supplies entered into customers’ accounting systems before 1 October 2019, if payment is made on or before 31 December 2019. The reverse charge will apply in all cases where invoices are entered into systems on or after 1 October 2019, or payment is made on or after 1 January 2020.

Further information and a flowchart can be found on HMRC’s website .

To discuss any of the points raised

Related news

VAT deferment

The Chancellor has announced that VAT for the period 20 March 2020 to 30 June 2020 will not need to be paid during this quarter.